As financial services become increasingly sophisticated, customers demand not only security but transparency and reliability—making trust the ultimate driver of success and resilience.

HSBC's $150M Failure of Zing: UX Lessons from a Banking App Collapse

Despite a significant investment of $150 million in its development, Zing failed within a year. And although the product didn't take off, those huge investments won't be wasted if the industry analyzes this case and learns from it properly.

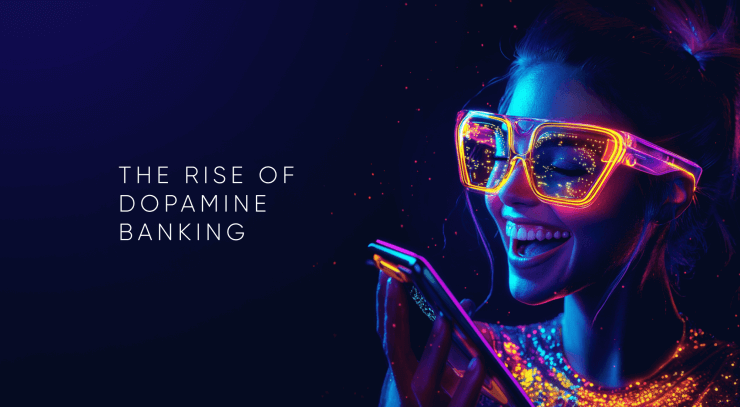

The Rise of “Dopamine Banking”: How Fintechs and Neobanks Are Redefining the Customer Experience

Fintech disruptors and neobanks are transforming finance with “Dopamine Banking”—where flashy visuals, gamified challenges, and social interactivity turn every tap into a rewarding experience. This blend of emotions and entertainment is reshaping how we view financial services.

UXDA’s DXG System for Building Strong Financial Brands Digitally

How can financial brands meet today’s user expectations? UXDA’s Digital Experience Governance framework offers a practical, actionable tool to help ambitious financial institutions create strong, future-ready digital brands.

Digital Transformation in Banking as a Branding Challenge

The most successful transformations in banking are not those that simply leverage technology, but those that seamlessly integrate powerful digital branding to create an emotional connection with customers.

Breaking Institutional Self-Deception to Improve Banking Customer Experience

Financial companies and banks worldwide are investing heavily to improve customer experience in banking. Despite these genuine efforts, many banks struggle to achieve the desired results. The culprit? Self-deception.

ChatGPT Prompts in Digital Banking and Fintech Product Design

This article unveils the secrets of using ChatGPT prompts to drive innovation in banking UX, providing insights into how this tool can be integrated into the standard design process for transformative results.

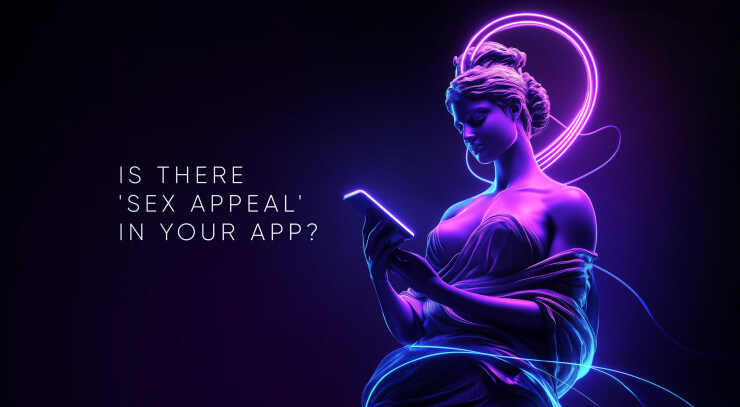

Role of Emotions in Banking CX: Is There Silent Revolution in Banking Services?

Successful banking apps like Revolut and Cash App thrive by creating sexy user experiences that go beyond basic functionality. In this article, we explore why injecting "sex appeal" into your financial product is the key to making it a market leader.

Digital Banking ROI: How Strategic Product Design Increases Bank Profits

As the financial industry evolves, digital products will remain central to a bank's identity and perception, making digital product design and UX key elements of banking strategy, brand identity, and profitability.

The Illusion of Completion in Banking Digital Transformation

The digital transformation of banking is an illusion—modernization will never truly end. Traditional banking, with branches and manual processes, is obsolete. To stay relevant, banks must operate like tech companies, driving continuous innovation and enhancing customer experience.