The traditional UX design approach may not be sufficient for the financial sector because it often focuses on surface-level interfaces and behavior patterns and is limited in addressing the complex, high-stakes nature of money. A systemic experience approach prioritizes long-term customer trust and emotional security over simple task completion or short-term conversion metrics. The systemic experience approach shifts UX from interface optimization to decision architecture in digital systems, aligning business objectives, brand intent, market context and customers’ needs.

By designing for high-stakes moments, failure scenarios and the full lifecycle of financial decisions, institutions reduce risk, protect trust and create durable customer value. Resilient experience architecture is the key to maintaining loyalty in an increasingly competitive and skeptical market.

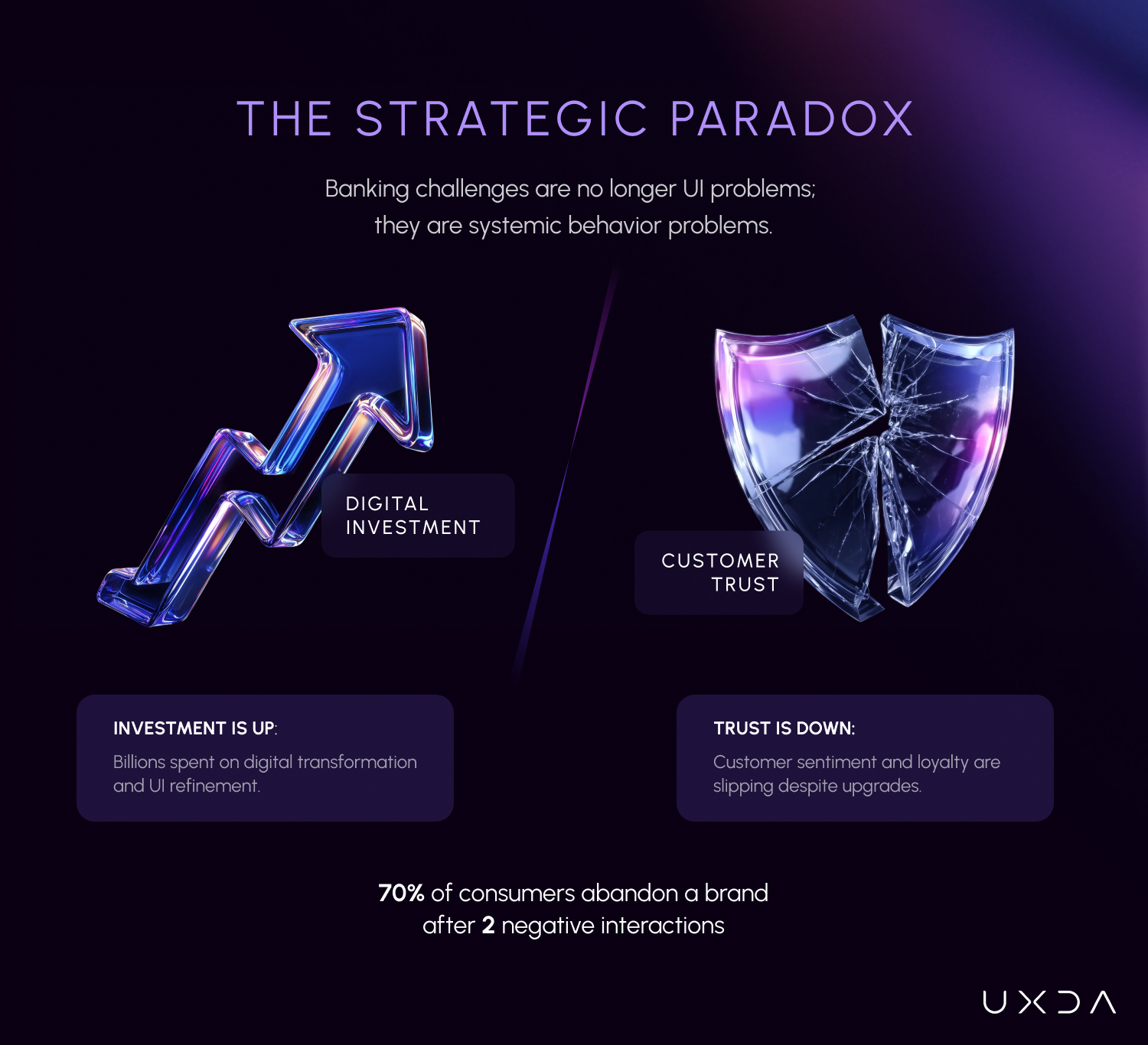

Financial institutions around the globe have spent years and billions refining user experience (UX) in their digital user interfaces (UIs). They’ve redesigned apps, simplified forms, optimized onboarding flows and run endless usability tests. Yet the same core issues persist in financial services UX: customer trust is eroding, support costs remain high, and users still panic or churn when things go wrong.

In short, traditional UX design is not fit to solve banking’s problems in full. This isn’t a failure of execution—it’s a failure of approach. Banking’s challenges aren’t UI problems at their core; they’re systemic behavior problems.

Financial institutions today face a stark reality: trust has become the primary driver of customer loyalty, but trust in banks is slipping despite expensive marketing and regular digital upgrades. Customers compare their financial apps not just against other competitors, but against every seamless digital experience in their lives.

Even one bad experience can send a customer running. Seventy percent of consumers say they’ll abandon a brand after just two negative interactions, and 25% will leave after only one. In an era when switching banks is easy and Fintech alternatives abound, a few UI tweaks, lean UX redesign or flashy new features won’t fix this. A deeper change in approach is needed.

Traditional UX is Not Created for Financial Services

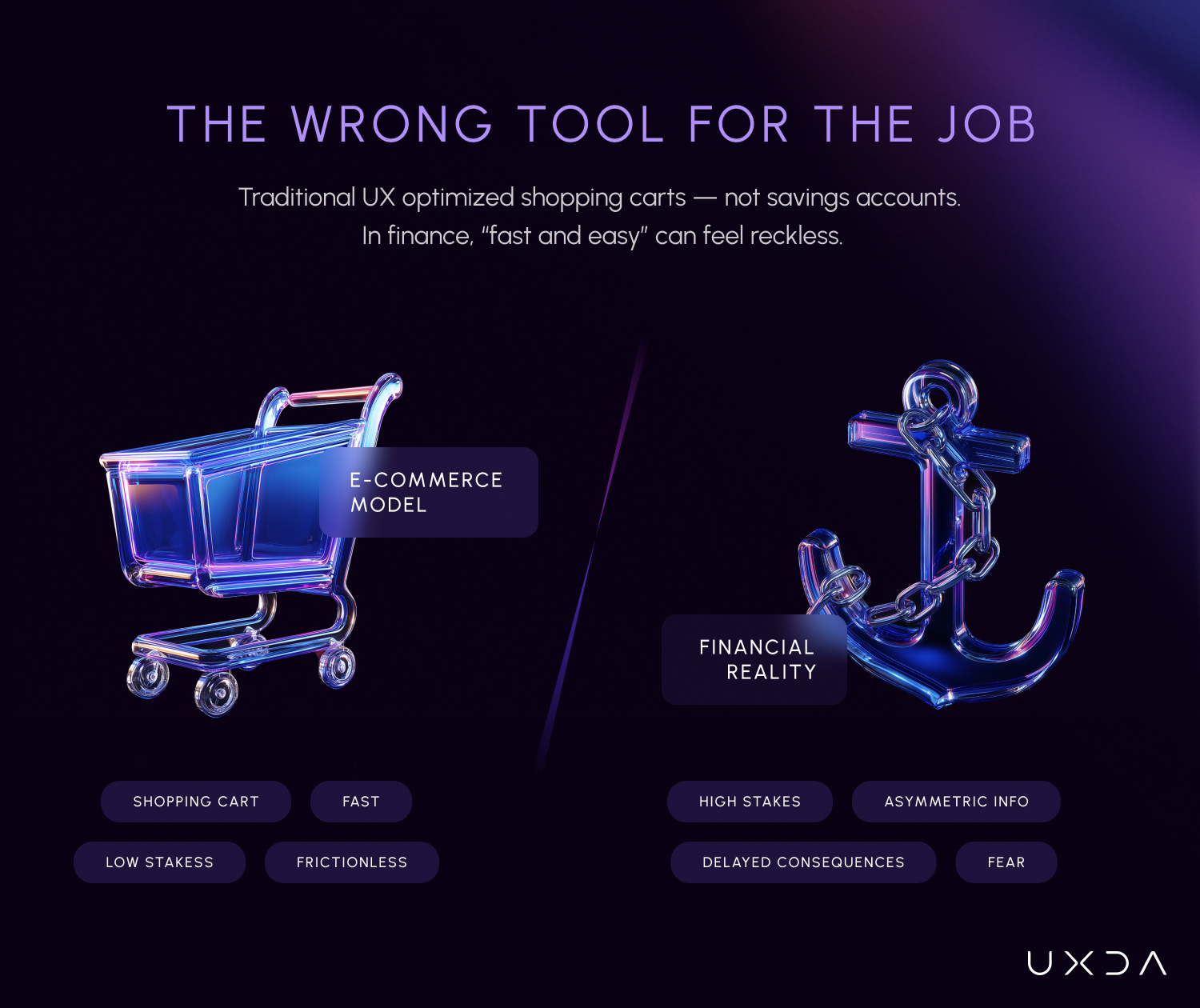

Traditional UX was born in a different world—a world of e-commerce, media platforms, SaaS tools, lean startups and digital task completion. In that world, UX effectively optimizes usability, speed, clarity, friction reduction and conversion. But financial services are fundamentally different. They deal with fear, uncertainty, delayed consequences, asymmetric information, irreversible decisions, legal responsibility, high failure cost—factors that extend far beyond a single screen.

When someone uses a banking product, they are not just “using an interface.” They are making decisions that could deeply affect their future. And traditional UX is not enough for that.

Traditional UX design tends to focus on individual touchpoints: making a screen or user flow as easy as possible in the moment. It asks, “How can we make this step or button more convenient for the user?” and often tackles problems reactively after the product is already defined.

Traditional UX in banking and financial services doesn’t fail because digital product designers lack skill. It fails because the scope of UX is narrowed. In financial organizations, UX design is usually isolated from the very things that define whether a financial service succeeds or fails.

Traditional UX practices often operate as if these elements are external or “out of scope”:

- Brand identity and value proposition

- Business strategy and financial goals

- Executive and cross-team alignment on UX strategy

As a result, UX optimizes inside a vacuum. Digital product screens improve. Flows get cleaner. But the financial service doesn’t become stronger on a strategic level.

For digital financial services, we need a holistic view. We should systematically apply a strategic UX design. It asks, “How does the entire system behave toward the user (and the business) over time and across long-term contexts?”

Instead of treating the interface as the center of the universe, strategic UX design treats the digital product, its UI and UX as just one part of a broader system. This system includes the user’s mindset, the brand identity and positioning, the digital ecosystem consistency, market context, the business model, technology constraints and opportunities, legal requirements and long-term impacts.

Traditional UX design is not wrong; making interfaces intuitive is necessary. The failure is that it’s not sufficient for financial services. Consider the unique nature of banking, investment and insurance products:

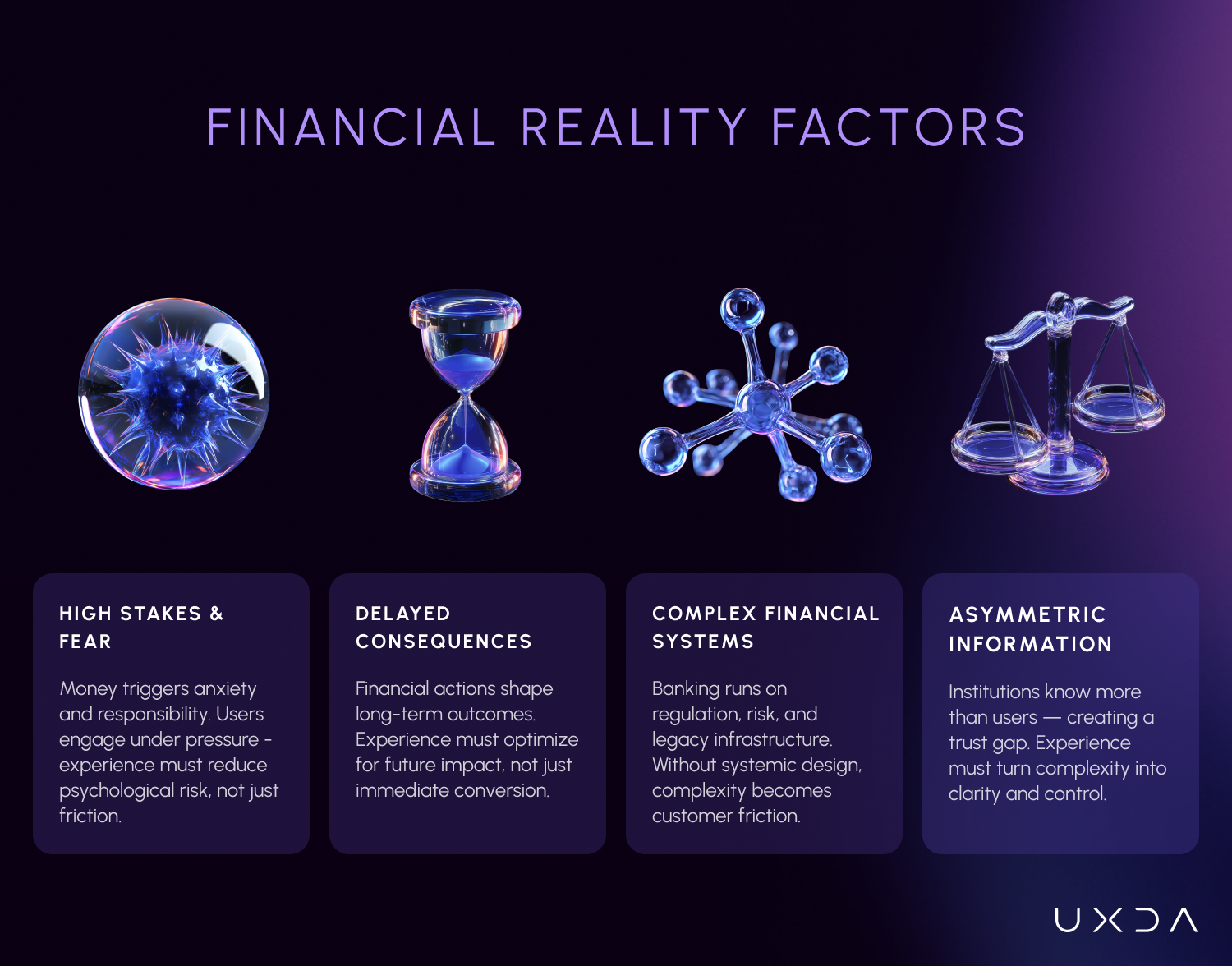

High Stakes Emotions

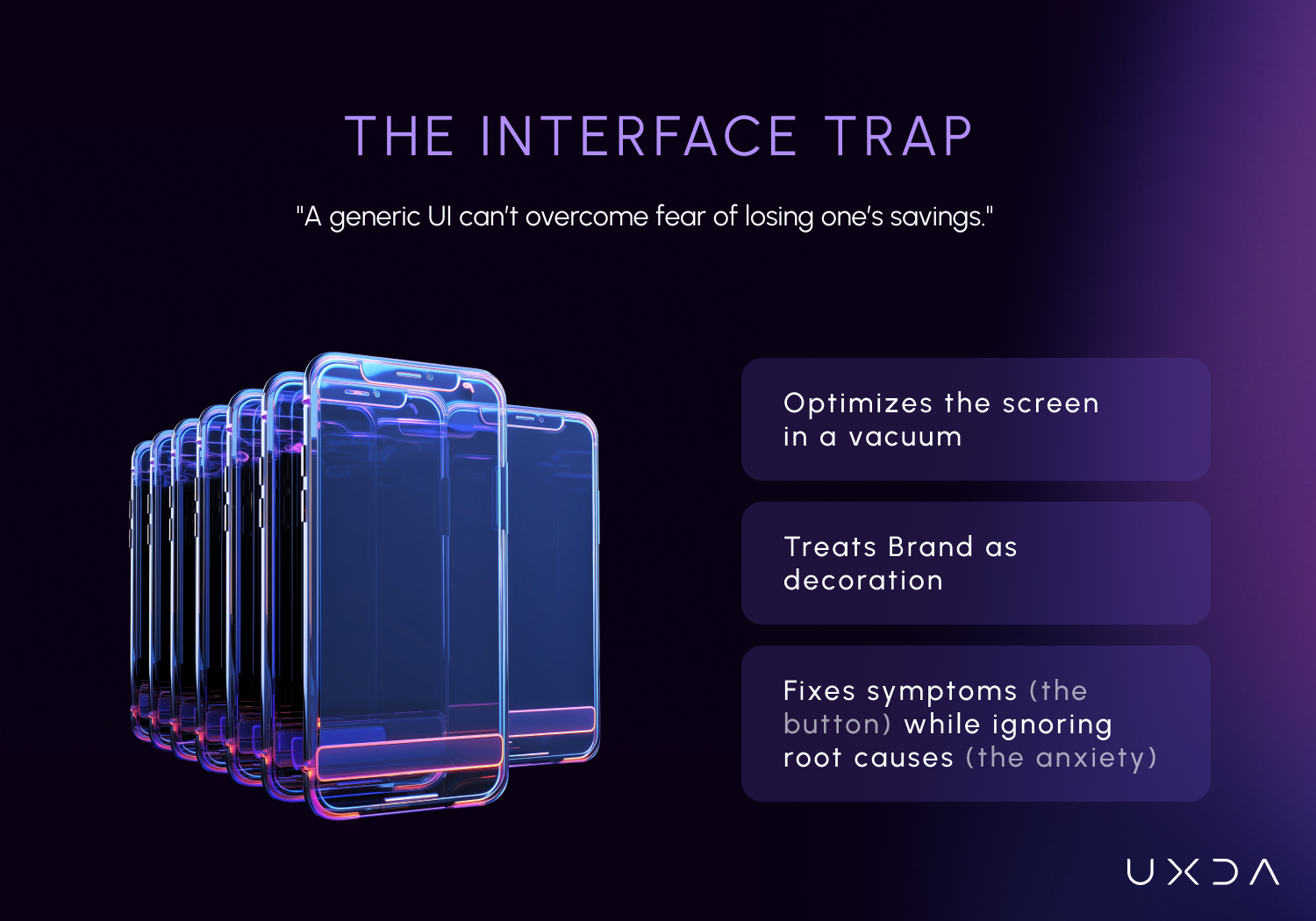

Money triggers deep emotions—anxiety, fear, greed, trust, regret. Users often approach financial interfaces with stress or skepticism. A generic UI can’t overcome the fear of losing one’s savings or confusion about a loan’s terms. Without designing for emotional states and cognitive biases, a financial app that’s “usable” in a lab can still feel intimidating or risky in real life.

Delayed Consequences

In finance, the real outcome of a user action often comes much later. Taking a loan, making an investment or missing a payment doesn’t show its full impact immediately. If UX is only optimizing the immediate transaction (e.g., “user successfully invested money in 3 clicks!”), it may ignore what happens afterwards—will this user regret their action in a year? Traditional UX tends not to own that question, but strategic UX must. Otherwise, it could lead to disaster. You will get good conversion but poor retention, or even backlash, when reality hits later.

Complex Large-Scale Systems

Financial products operate within complex systems (e.g., hundreds of features, trillions of transactions, risk models, fraud detection, regulatory compliance like KYC/AML, etc.) that sometimes override or alter the user’s experience. For example, a fraud system might block a user’s transaction unexpectedly, or a regulation system might mandate extra steps. If the UX is not designed systemically, experiences will feel like random, frustrating disruptions that ruin customer satisfaction. A user who gets a cryptic “transaction denied” message because of an unseen risk rule will blame the bank. Traditional UX might consider that an edge-case error message. Systemic UX treats it as an inevitable scenario to design for.

Trust and Asymmetry

There’s an inherent information asymmetry in finance—the institution knows more about the rules and the fine print than the user does. Traditional UX often fails by either overwhelming users with information or hiding it entirely. Neither builds trust. Systemic design looks for a balance: how to be transparent and supportive, giving users control without burdening them with complexity. In banking, trust is UX—if your user interface is clear and human, users perceive the service as safer and more reliable. A fancy new feature won’t matter if customers don’t feel secure and respected when using it.

Given these factors, it’s clear why an interface-focused UX design falls short in financial services. Banks often see a paradox: “We improved our app’s design, but customers still don’t engage more, and they still drop off when stressed.” The problem isn’t the UI details; it’s the underlying experience architecture.

Banks have poured billions into digital tools, yet trust continues to slip because customers are left feeling confused and unsafe when journeys get complicated. The solution is not more features or visual polish—it’s a systemic change in how digital experiences are conceived.

Where Traditional UX in Financial Services Breaks Down

A traditional UX design question in banking might be, “How can we make this screen or feature easier to use right now?” A strategic UX question is, “How can we ensure the entire system is helping the user and the business make the right choices—today, tomorrow and next year?”

The difference is profound. One optimizes the interface, and the other optimizes the interaction between the user and the product at a system level. The systemic approach doesn’t replace good interface design—it builds upon it, expanding the designer’s focus from isolated moments to the complete user relationship.

1. It Treats UX as a Support Function, Not as a Strategic Large-Scale Control System

The most fundamental failure of traditional UX in banking and financial services is not methodological—it is positional. UX is treated as a service function that executes requirements and improves digital product interfaces after decisions have already been made. It is invited in once a direction is set, the scope is fixed, and constraints are locked. But in financial organizations, experience is not an outcome of strategy—it is one of the primary ways strategy is executed and controlled. How risk is communicated, how responsibility is shared, how trust is built, how behavior is guided—these are not design details; they are strategic layers.

Traditional UX tends to be tactical and reactive. It addresses immediate pain points. For example, “Users aren’t clicking the CTA; let’s make the button bigger or change the copy.” It often fixes symptoms as they arise (e.g., usability issues, confusing labels, low conversion steps).

Systemic UX is strategic and proactive. It aims to prevent problems before they start by understanding the root causes. Rather than asking, “Why aren’t users clicking this?” systemic designers ask, “Why did users reach a point of hesitation in the first place, and how can we re-architect the experience to avoid that doubt?” The focus shifts from local optimizations to global effects. For example, instead of just boosting the click rate on a feature, a systemic approach might realize the feature itself causes user anxiety and find a way to eliminate the anxiety and not just tweak the UI.

When UX is positioned as downstream execution instead of upstream control, banks lose their ability to steer customer behavior intentionally. Strategic UX treats experience and design as a large-scale control and execution system that shapes decisions, mitigates risk, enforces values and translates digital strategy into everyday behavior at scale. Without this shift, all UX improvements remain tactical, fragile and easily overridden.

2. It Operates Detached from Business Strategy and Risk Reality

Traditional UX in banking is often driven by good intentions: reduce friction, increase engagement and simplify flows. But in financial organizations, these goals cannot exist in isolation. Every UX decision has implications for cost-to-serve, regulatory exposure, risk appetite and long-term value creation. When UX is designed without explicit connection to business strategy and processes, it becomes locally optimized and systemically expensive.

Features that increase engagement may increase support costs. Simplified flows may increase risk exposure. Well-intended improvements can directly contradict strategic priorities. Without strategic guardrails, UX turns into a collection of disconnected optimizations instead of a coherent value system aligned with how the financial institution actually makes money and manages risk.

3. It Ignores Brand Identity and Value Proposition

In many banks and financial organizations, brand is treated as a marketing asset while UX is treated as a product discipline. Campaigns promise care, stability, transparency or premium service, yet digital products behave in generic, mechanical ways. The result is a silent contradiction. The brand sounds human, but the app feels cold. The brand claims trust, but the digital experience feels defensive.

Traditional UX often sees brand as a decoration—colors, typography, tone of voice—rather than as a behavioral contract. In banking, the brand is not what you say. It is how the system behaves under pressure. When digital experiences fail to embody the bank’s identity and value proposition, the strongest brand promise disappears the moment the user opens the app.

4. It Lacks Executive and Cross-Team Alignment on Experience Strategy

In large financial organizations, UX rarely fails because of disagreement among teams. It fails because there is no shared experience logic guiding decisions. Business, compliance, risk, product, marketing, development and design each optimize for their own objectives, revisiting the same decisions again and again. Redesigns happen frequently, but nothing fundamentally changes.

Traditional UX treats alignment as a communication problem, solved through workshops and documentation. In reality, it is a decision-system problem. Without a shared definition of what the experience is meant to achieve, every trade-off becomes a debate, and every roadmap becomes unstable. Hence, UX design becomes a short-term project instead of an operating system.

5. It Produces Artifacts, not Systems

Traditional UX is very good at producing insights, wireframes, prototypes and features. What it often fails to produce is clarity about how product decisions should be made when priorities conflict. When speed conflicts with safety, when conversion conflicts with trust and when growth conflicts with responsibility, teams fall back on opinions and politics.

For example, in traditional workflows, teams often build feature after feature—designing and testing each new screen or function in isolation. The mindset is feature → screen → usability test → iterate. Not enough attention is given to how these features interrelate or what behavior emerges from their combination. Systemic UX treats connections and interactions over time as first-class design elements.

When adding or changing a feature, systemic designers ask: How will this affect other features? How will it shape user behavior, not just today but after weeks or months of use? What are the impacts on customer support? On churn rates? On user trust and brand perception? On compliance or risk? In this view, UX design becomes the engineering of relationships and dynamics systems, not just the drawing of screens. It’s about designing the behavior of the system.

Traditional UX knowledge exists, but it does not govern systemic behavior. Over time, decisions drift away from original intent. A strategic UX approach turns experience intent into decision rules that guide trade-offs consistently across teams and over time. Without this, even a strong UX stack slowly erodes as the organization scales.

6. It Chases Short-Term Metrics and Measures Success Too Early

Traditional UX optimizes for what is easy to measure: conversion, activation, task speed and immediate success rates. On paper, this looks efficient. In reality, it creates long-term damage. Banks that adopt this approach later wonder why churn increases, support costs explode, complaints grow, and non-performing loans rise. The issue is not that UX failed, but that UX impact was measured at the wrong time horizon.

A successful banking experience cannot be evaluated in a single session. It must be measured across the full customer journey—entry, daily usage, moments of stress and recovery after mistakes. When UX is judged too early, it optimizes short-term wins while creating long-term losses.

7. It Optimizes Screens, not Consequences

Most traditional UX in banking focuses on the moment of interaction. Can the user complete the task? Is it fast? Is it clear? Success is defined by whether the task ends without friction, but the real impact of financial decisions does not happen on the screen. It happens months or even years later.

A credit taken today becomes stress later. An investment made today becomes panic during a market drawdown. A mistaken payment results in anxiety and loss of control. An unpaid bill results in penalties. Excessive spending quietly leads to shortage. Traditional UX celebrates completion. Banking reality lives in consequences, uncertainty and long-term financial risks.

A traditional UX mindset often just “treats the symptom.” If there’s low conversion, high drop-off or user confusion, the response is to tweak the UI element causing friction (e.g., simplify text, add a tooltip, insert a progress bar, etc.).

These can be valid fixes, but they might only mask deeper issues. That's why the most complex services have the largest instructions. Systemic UX digs into root causes behind user behaviors. Is a low conversion really due to a confusing screen, or is it because the user fundamentally distrusts something about the process? Is a high drop-off rate a UI issue, or does it indicate cognitive overload or misaligned incentives?

Systemic designers address problems like cognitive overload, conflicting user motivations, lack of trust, poor choice architecture or a disconnect between what the product promised and what it delivers. By solving the underlying cause, you eliminate the symptom more effectively than any quick UI patch could.

System-driven UX focuses on the entire ecosystem of interactions. The question isn’t just “Can the user complete this task easily?” but “How does the business ecosystem as a whole behave toward the user, the market and within its context?”

8. It Treats Errors and Uncertainty as Exceptions

In traditional UX thinking, errors are treated as edge cases. They are assumed to be rare, handled with generic messages and a fallback to support. But in financial services, errors are not exceptions—they are the experience. Fraud blocks are normal. Cross-bank transfers are delayed. Transactions remain pending. Verification fails. Limits are exceeded. Uncertainty is constant.

When these moments are not designed as first-class experiences, trust collapses instantly. A perfect success flow cannot compensate for a single poorly handled failure when money is involved. In banking, the error screen often matters more than the success screen.

Traditional UX often fixates on the here and now—the first-time use, the immediate session. Success is measured by task completion today. Strategic UX builds in time as a key dimension of design. It considers the user’s entire journey: onboarding → ongoing use → moments of error or crisis → recovery → long-term habit formation and retention.

A systemic approach will deliberately design for future scenarios—the first week of use, the first time something goes wrong, the moment a user contemplates quitting the service and even the conditions under which they return. It’s not just about designing a “happy path” but designing resilience and trust into the experience over time.

9. It Pushes Responsibility to the User

If you read most banking interfaces carefully, a pattern appears: “Invalid input.” “Operation failed.” “Try again later.” The language may be neutral, but the message is clear: the user is at fault. Traditional e-commerce UX assumes responsibility ends once instructions are clear. But when people’s finances are involved, this approach destroys confidence.

Users do not want to feel blamed when money is delayed, blocked or lost. A financial system must take responsibility by design—by explaining what happened, why it happened, what will happen next and how the user is protected. When UX shifts responsibility onto the user, trust breaks forever at the most critical moments.

10. It Ends at Delivery and Ignores Governance Over Time

The output of traditional UX efforts is typically a more usable interface—cleaner layout, smoother flows, higher immediate conversion or satisfaction scores. These are valuable, but often fragile wins. A nicely designed app can still fail if it doesn’t fit into users’ lives or if it ends up breaking their trust later.

Often, traditional UX treats a digital product launch as the finish line. After delivery, experiences are left to evolve through incremental changes, urgent fixes and new features. Over time, consistency breaks down, brand weakens, and digital complexity grows. Redesigns are triggered not by strategy shifts, but by accumulated incoherence.

In banking and financial services, where trust is built through consistency over years, this decay is costly. Without governance and ongoing calibration, UX value leaks silently. Strategic UX recognizes that experience is a living system that must be protected, measured and recalibrated continuously week-by-week—not redesigned every five years from scratch.

The outcome of strategic UX is a sustainable, constantly upgraded product. It means higher user trust and loyalty because you designed with transparency and empathy from the start and keep feedback loop post-launch. It means constantly avoiding hidden “UX debt”—those design shortcomings that quietly undermine metrics until they become crises.

Ultimately, a systemic approach to UX design aims for predictable growth in real business metrics (e.g., retention, lifetime value, lower support burden, etc.) by ensuring the product and the user are on the same side over the long run, not at odds.

What is the Systemic UX Approach in Financial Services?

Systemic UX in financial services applies system thinking to experience design, shifting the focus from individual screens or features to the entire ecosystem in which a financial product operates—users, technology, policies, processes and organizational decisions. Rather than fixing surface-level usability issues, it addresses the upstream structures that shape behavior, risk and trust over time.

Unlike traditional UX, which optimizes isolated touchpoints, systemic UX designs for how the whole system behaves under real conditions, including scale, failure and change. It shapes the system's behavior across states and time, rather than just how a screen is structured. This approach is essential in complex domains such as finance, where experience outcomes are driven as much by internal logic and governance as by interface quality.

We have the following key principles of systemic UX in financial services:

The Whole is Greater Than the Sum of its Parts

Digital experience is a system, not a screen. You can’t understand a system by optimizing individual components in isolation. A financial experience is shaped by brand perception, cross-channel digital communication, usability consistency, overall visual language, range of features and usability, policies, risk rules, disclosures, support processes, pricing, tone of voice, etc.—not the user interface alone. Optimizing interfaces without aligning the system creates false clarity.

Everything is Interconnected

Actions in one part of the system ripple elsewhere, often in unexpected ways. Cause and effect are rarely linear or immediate. Every design decision has risk and trust consequences, and even small changes can create global improvements or global problems. Changes to flows, defaults, limits or messaging alter customer behavior—and therefore financial risk, support load and trust levels—often weeks or months later.

Focus on Relationships, Not Just Elements

What matters most is not the components themselves, but how they interact, reinforce or constrain one other. Relationships matter more than features, because what customers experience in financial services is the relationship between product logic, communication and consequences over time—not isolated features or journeys.

Feedback Loops Shape Customer Behavior

Systems are shaped by reinforcing loops (that amplify outcomes) and balancing loops (that stabilize or resist change). Ignoring feedback leads to recurring failures. Poorly designed alerts, limits or error handling train customers to panic, overload support or disengage. Well-designed feedback builds confidence and self-regulation in self-serve digital financial products.

Delayed Effects are the Norm in Finance

Effects often appear long after decisions are made. Short-term success can hide long-term damage. In finance, consequences surface after the interaction: fees, rejections, investment losses, budget deficits or compliance events. UX must anticipate these delayed moments, not just the point of action.

Structure Determines Outcomes

System behavior is largely a product of underlying structures—rules, incentives, flows and constraints—not individual intent or effort. Legacy operating systems, bureaucratic protocols, legal procedures, approval logic and compliance constraints often define the real experience in finance. If these are misaligned, no amount of visual polish can fix the outcome.

Optimize for the System, Not for Silos

Improving one function, metric or team can degrade overall performance if system-level goals aren’t aligned. When channels, products or teams in financial institutions optimize independently, customers experience friction, inconsistency, contradictions, confusion and loss of trust—especially in key moments of stress.

Leverage Points Sit in Behavior Design, Not Decoration

Well-placed interventions at leverage points can reshape the entire system, while large efforts in the wrong place do nothing. Small changes in defaults, framing, timing or responsibility-sharing can dramatically reduce risk and increase trust—far more than superficial UI redesigns.

UX Maturity Model: Financial Institutions’ Path to Institutionalized User Experience

As we stated previously, in banking, user experience is not a matter of convenience. It shapes how customers perceive risk, decide under uncertainty and place long-term trust in institutions. A single unclear interaction can trigger panic and support escalation, reputational damage or regulatory scrutiny long after the moment of use.

Yet most financial institutions still treat UX as a downstream delivery activity—applied after strategy, compliance and technology decisions are already fixed. This creates a structural gap: interfaces improve, but the system governing customer behavior remains unchanged.

UX maturity determines whether an experience is reactive or controlled, dependent on individuals or embedded institutionally, optimized for short-term metrics or long-term trust. Without maturity, banks accumulate invisible experience debt. With it, they gain predictability, resilience and trust at scale.

UXDA does not treat UX maturity as a design evolution. It treats it as a systemic transformation. Through the DXG system (Digital Experience Governance), UXDA connects business strategy, brand values and digital experience behavior—how customers are guided, informed, protected and supported in real financial moments.

The objective is not to replace existing processes, but to embed experience logic into how financial institutions already operate—across product, risk, compliance, operations and leadership. The outcome is not better design maturity, but institutional experience maturity.

Matured UX in financial institutions is not a one-time redesign project. It is an ongoing value management and control system.

Level 1 — Ad-Hoc UX

“We redesign when something breaks.”

UX exists as a reactive intervention. Design work is triggered by complaints, declining metrics, competitive pressure or rebranding initiatives. UX teams are execution-focused and invited late, once strategy, scope and constraints are already fixed. Experience quality depends on individual talent, not institutional rules.

How UX Shows Up

- One-off redesign projects

- Usability testing at the end of delivery

- UX success measured by UI clarity or task completion

- UX seen as a cost or cosmetic improvement

What Really Happens

- Each product optimizes locally

- Inconsistencies multiply across channels

- Risk is “disclosed,” not understood

- Trust issues appear months after launch

Hidden Risk

Experience debt accumulates silently. Problems surface only when customers panic, churn or escalate.

Level 2—Systemic UX

“We don’t leave experience to chance anymore.”

UX is recognized as a strategic and systemic discipline, not just an interface design service. The organization introduces experience principles, review mechanisms and shared standards. UX begins to influence decisions earlier—though not yet consistently across the institution. Governance exists, but it is still partially dependent on people and projects.

How UX Shows Up

- Overall UX strategy

- Defined experience principles and design systems

- Regular UX evaluations and reviews

- UX involvement in product planning

- Cross-team alignment on UX

- UX consistency across the digital ecosystem

What Changes

- Subjective design debates become structured discussions

- Obvious experience risks are identified earlier

- Consistency increases across products

- UX starts speaking the language of business and risk

Structural Limitation

Systemic UX governance often exists around the organization, not inside it. When priorities shift or key people leave, digital experience quality can still drift.

Level 3—Institutionalized UX

“Experience is how we run the business.”

UX is embedded as a control system within the organization. Digital experience priorities and principles are non-negotiable. Decision frameworks are formalized. UX accountability is distributed across roles—product, risk, compliance, content, support and leadership. UX no longer depends on individual teams; the system enforces itself.

How UX Shows Up

- UX mandate aligned with business, brand and risk strategy

- Experience reviews integrated into governance processes

- Clear UX accountability at executive and operational levels

- Continuous experience health monitoring

- External partners act as auditors and stewards, not just executing vendors

What Becomes Possible

- Trust scales across products and channels

- Digital experience remains stable during growth, crises and change

- Redesigns become controlled evolution, not emergency fixes

- UX outlives teams, vendors and technologies

Strategic Advantage

The institution does not just design better experiences. It prevents bad experiences from being created.

Conclusion: From Interface Design to Relationship Design

Traditional UX has helped financial institutions make digital interfaces cleaner, faster and easier. But finance is not a “task-completion” industry. It’s a life-impact industry. People don’t come to a financial app just to use it—they come to make decisions under uncertainty, to hand over responsibility, to feel safe when stakes are real. In that context, usability is not the finish line; it’s the entry ticket.

In financial services, UX can no longer be just about making things easy or pretty—it must be about making things right and resilient. Traditional UX design asks, “How do I make this interface convenient?” Systemic UX asks, “How do I ensure this entire service lives up to its promise to the user and the business over time?”

This shift in mindset is no longer optional. As industry research and consumer behavior both show, trust is the currency of banking in the digital age. Customers will quickly abandon even the most feature-rich app if it makes them feel insecure or unsupported for a moment. On the other hand, a thoughtful, systemic experience can turn users into loyal advocates, even if it means sometimes doing less or slowing down in the short term.

Investing in systemic UX is investing in the longevity of your customer relationships. It’s moving from a transactional mindset (“Did the user complete task X today?”) to a relationship mindset (“Will the user trust us with their money tomorrow?”). The former might win the quarter, but the latter wins the decade.

![]()

Digital financial services isn’t about transactions; it’s about trust over time. And trust isn’t built by a single screen or a one-off delight moment. It’s built by an entire system consistently behaving in the customer’s best interest, even (and especially) when things go wrong.

What financial services needs is a shift from designing screens to designing behavior. From “making it easy to do” to “making it safe to decide.” From single-touchpoint improvements to a continuously governed experience system that aligns product, risk, brand promise, support and long-term customer outcomes.

If traditional UX made banking and other financial services apps usable, strategic UX makes financial services valuable—as in valued by users as their go-to financial partner. The future of financial UX will be won by those who design relationships, not just interfaces. And that means thinking systemically, acting holistically and always, always considering the human on the other side of the screen as a partner in a long-term brand journey.

That requires institutionalizing a systemic approach—not as a one-off project, but as an operating model: a shared experience logic that guides trade-offs, shapes responsibility, designs for uncertainty and protects consistency as the organization evolves. Because in modern financial services, digital experience is not a layer on top of strategy. It is the strategy in action— every day, at scale.

Discover our clients' next-gen financial products & UX transformations in UXDA's latest showreel:

If you want to build a strong competitive advantage through strategic UX and digital experience systems, talk to UXDA. We empower financial organizations to scale experience systems that align business strategy, digital products, and customer needs — enabling sustainable growth, clear differentiation, and long-term customer value through emotionally intelligent digital experiences.

- E-mail us at info@theuxda.com

- Chat with us in Whatsapp

- Send a direct message to UXDA's CEO Alex Kreger on Linkedin